Q. Discuss the relevance of ‘Risk Management’. What are the steps involved in the Risk Management process?

Risk

management is a critical process for any organization, regardless of size or

industry. It's not merely about avoiding negative outcomes; it's about

proactively identifying, assessing, and mitigating potential risks to achieve

objectives, protect resources, and enhance overall performance. In essence,

risk management is about making informed decisions in the face of uncertainty. Its

relevance spans every facet of an organization, from strategic planning and

financial management to operational efficiency and project execution. Without a

robust risk management framework, organizations are vulnerable to unforeseen

events that can disrupt operations, damage reputation, and even threaten their

survival.

The

modern business environment is characterized by increasing complexity,

volatility, and interconnectedness. Globalization, technological advancements,

evolving regulatory landscapes, and geopolitical uncertainties all contribute

to a heightened level of risk. In this dynamic context, effective risk

management is no longer a luxury but a necessity for sustainable success.

Here's a deeper look at its relevance:

- Strategic Decision-Making: Risk management provides a structured approach to

evaluating the potential impact of various strategic options. By

identifying and assessing the risks associated with different strategies,

organizations can make more informed choices that align with their overall

goals and risk appetite. It helps to prioritize initiatives, allocate

resources effectively, and develop contingency plans.

- Protecting Assets and

Resources: Organizations invest

significant resources in physical assets, intellectual property, human

capital, and financial resources. Risk management helps to safeguard these

assets by identifying potential threats such as natural disasters,

cyberattacks, fraud, and operational disruptions. By implementing

appropriate controls and mitigation strategies, organizations can minimize

losses and ensure business continuity.

- Enhancing Operational

Efficiency: Risks can significantly impact

operational efficiency by causing delays, errors, and cost overruns. Risk

management helps to identify bottlenecks, streamline processes, and

implement quality control measures to minimize operational disruptions and

improve productivity. It fosters a proactive approach to problem-solving

and continuous improvement.

- Improving Project Outcomes: Projects are inherently risky due to uncertainties

related to scope, budget, timeline, and resources. Risk management is

essential for successful project execution. It enables project managers to

identify potential roadblocks, develop mitigation plans, and proactively

manage risks throughout the project lifecycle. This increases the

likelihood of delivering projects on time, within budget, and to the

required quality standards.

- Ensuring Business Continuity: Unexpected events such as natural disasters,

pandemics, or supply chain disruptions can severely impact business

operations. Risk management plays a vital role in ensuring business

continuity by developing disaster recovery plans, establishing backup

systems, and implementing crisis communication protocols. This allows

organizations to quickly recover from disruptions and minimize downtime.

- Protecting Reputation and Brand

Value: Negative events such as

product recalls, data breaches, or ethical lapses can severely damage an

organization's reputation and brand value. Risk management helps to

identify and mitigate reputational risks by implementing ethical

guidelines, ensuring product safety, and protecting customer data. It

fosters a culture of transparency and accountability.

- Compliance with Regulations: Many industries are subject to various regulations

related to safety, environmental protection, data privacy, and financial

reporting. Risk management helps organizations to identify and comply with

these regulations, avoiding penalties and legal liabilities. It ensures

that the organization operates within the legal and ethical framework.

- Improving Stakeholder

Confidence: Investors, customers,

employees, and other stakeholders are increasingly concerned about risk

management practices. Organizations with robust risk management frameworks

are viewed as more stable, reliable, and trustworthy. This enhances

stakeholder confidence and can lead to improved access to capital,

stronger customer relationships, and increased employee engagement.

- Competitive Advantage: Organizations that effectively manage risks are better positioned to seize opportunities and adapt to changing market conditions. They are more agile, resilient, and innovative. This can provide a significant competitive advantage in the marketplace.

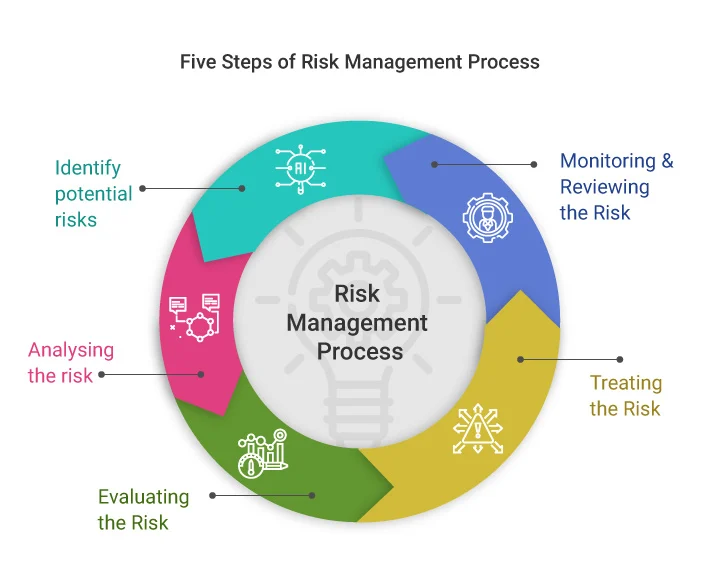

Steps Involved in the Risk Management Process:

The

risk management process is a systematic and iterative cycle that involves

several key steps:

1.

Risk

Identification: This is the crucial first step

where potential risks are identified and documented. It involves brainstorming,

conducting surveys, analyzing historical data, and consulting with experts to

identify anything that could potentially impact the organization's objectives.

Risks can be categorized in various ways, such as strategic, operational,

financial, compliance, reputational, and technological. It's important to

consider both internal and external risks. Techniques like SWOT analysis,

PESTLE analysis, and risk registers can be helpful in this stage.

2.

Risk

Analysis: Once risks are identified, they

need to be analyzed to understand their potential impact and likelihood of

occurrence. This involves assessing the severity of the consequences and the

probability of the risk event happening. Qualitative methods, such as risk

matrices, can be used to categorize risks based on their impact and likelihood.

Quantitative methods, such as Monte Carlo simulations, can provide more precise

estimates of risk exposure.

3.

Risk

Evaluation/Assessment: This step

involves prioritizing risks based on their level of significance. Risks with

the highest potential impact and likelihood are given the highest priority.

This helps organizations to focus their resources on managing the most critical

risks. Risk appetite, which is the level of risk an organization is willing to

accept, plays a crucial role in risk evaluation.

4.

Risk

Response/Mitigation: Once risks are evaluated,

appropriate risk responses need to be developed and implemented. There are

several common risk response strategies:

o Avoidance:

This involves eliminating the risk altogether by ceasing the activity or

project that gives rise to the risk.

o Reduction:

This involves taking steps to reduce the likelihood or impact of the risk. This

can be achieved through implementing controls, improving processes, or

diversifying resources.

o Transfer:

This involves shifting the risk to a third party, such as through insurance or

outsourcing.

o Acceptance:

This involves acknowledging the risk and making a conscious decision to accept

it without taking any action. This may be appropriate for low-impact,

low-likelihood risks.

5.

Risk

Monitoring and Review: Risk

management is an ongoing process. Risks need to be continuously monitored and

reviewed to ensure that the risk responses are effective and that new risks are

identified. This involves tracking risk indicators, conducting regular risk

assessments, and updating the risk management plan as needed. Regular reporting

on risk management activities is also essential.

6.

Communication

and Consultation: Effective communication and consultation

with stakeholders are crucial throughout the risk management process. This

ensures that everyone is aware of the risks and the risk management strategies

that are being implemented. Stakeholder input can also be valuable in

identifying and assessing risks.

7.

Documentation

and Reporting: Maintaining proper documentation of

the risk management process is essential for accountability and continuous

improvement. This includes documenting the identified risks, the risk analysis,

the risk responses, and the monitoring activities. Regular reporting on risk

management activities to senior management and other stakeholders is also

important.

Integrating

Risk Management:

For

risk management to be truly effective, it needs to be integrated into the

organization's culture and decision-making processes. This requires strong

leadership support, clear communication, and training for all employees. Risk

awareness should be embedded in all aspects of the organization's operations,

from strategic planning to day-to-day activities.

Continuous

Improvement:

The

risk management process should be continuously reviewed and improved. Lessons

learned from past risk events should be captured and used to update the risk

management framework. Organizations should also stay abreast of emerging risks

and adapt their risk management strategies accordingly.

In

conclusion, risk management is an essential process for any organization

seeking to achieve its objectives, protect its resources, and thrive in an

increasingly complex and uncertain world. By implementing a robust risk

management framework, organizations can make informed decisions, minimize

losses, enhance operational efficiency, and build stakeholder confidence. It's

not about eliminating all risks, which is often impossible, but about

understanding and managing them effectively to maximize opportunities and

achieve sustainable success.

0 comments:

Note: Only a member of this blog may post a comment.